Comprehending the strength of the U.S. economic recovery from the Great Recession is a priority for the Federal Reserve as it continues to weigh whether an interest rate hike is appropriate and how it may affect future growth.

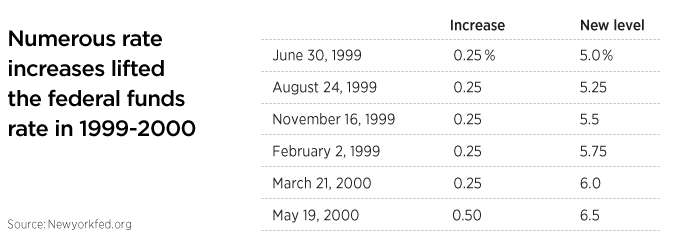

Rate increases have typically come in response to economic strength. This was the case in 1999-2000, when the Fed raised rates several times to temper inflationary pressure.

The U.S. economy posted robust growth numbers in the late 1990s, reaching GDP growth rates of 4.5% in 1997, 4.4% in 1998, and 4.7% in 1999 (Source: worldbank.org). In the same years, inflation remained fairly tame at 2.3%, 1.6%, and 2.2%, respectively. But the pick up in inflation between 1998 and 1999 caught the Fed’s attention, as did a string of record highs for the stock market, signaling possible “irrational exuberance” in stock prices, a concern that Fed Chair Alan Greenspan had raised in prior years.

The Fed considered raising rates in 1998, but chose not to make a move amid concerns about the impact of global events such as the Asian financial crisis and Russian default.

In 1999, however, the Fed decided to act. From June 1999 through July 2000, the Fed raised interest rates six times. During the period, the federal funds rate went from 4.75% to 6.5%.

On June 30, 1999, the Fed raised the federal funds rate by 25 percentage points to 5.0%.

Amid the rate increases, the stock market corrected. Prices began to tumble in July 1999, and the downturn lasted through October 1999, when stocks rebounded and finished the year with a strong rally.

In 2000, Fed rate hikes continued in February and March, bringing the federal funds rate to its highest level in nearly five years. Initially, stocks held up. The S&P 500 Index rose to 1,493.87, setting a record in March.

However, the issue of inflated stock valuations, particularly in the technology sector, remained a concern. Many stocks in the so-called ‘new economy’ or dot.com segment included start-up companies with weak revenues but generous market valuations. Fears about inflation also emerged when the CPI jumped 0.7% and core CPI rose 0.4% in March.

The dot.com bubble burst in March, beginning with a huge selloff in the Nasdaq. The Dow Jones Industrial Average and Nasdaq both experienced record-setting declines.

The final rate hike for the cycle came on May 16, 2000, with an increase of 50 percentage points to 6.5%. GDP growth slowed significantly in the third quarter.

By the beginning of 2001, the slowdown forced the Fed to reverse course and begin cutting rates. In a hasty retreat, the Fed cut rates by a full percentage point in two moves during January 2001. The Fed would follow with nine more cuts during the course of the year, bringing the federal funds rate down to 1.75%.

As the Fed was frantically slashing rates, the economy and stock market continued on their downward paths. In 2001, the United States entered a recession, bringing to an end its longest post-war economic expansion. The recession was relatively brief, lasting from March to November of 2001. For stocks, however, the consequences were more severe. Large-cap stocks continued to slump even after the economy began to recover. In sum, the S&P 500 Index posted negative results for three straight years: in 2000, amid the rate hikes; in 2001, amid the recession; and in 2002, in the early months of the recovery.

Fixed-income markets, on the other hand, fared better, as bullish conditions for high-quality assets continued.

298375